- Position:

- Home

- English Home

- Investor Relations

- Management Policy

- Japan Post Group Internal Audit System

Japan Post Group Internal Audit System

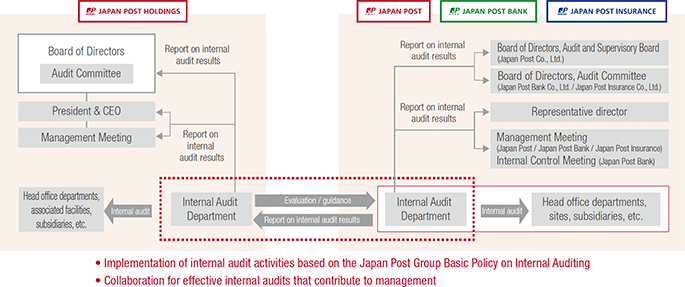

The Japan Post Group has established an effective internal audit system at each Group company in order to ensure sound administration and proper operations aimed at building customers' trust. We are particularly focused on ascertaining the challenges identified by frontline employees at post offices and other such locations, as well as enhancing coordination among the Group's internal audit departments.

Internal audit system framework

Based on the Japan Post Group Basic Policy on Internal Auditing, which outlines the basic views to internal audits conducted by each Group company, we have established an effective internal audit system framework befitting the nature of their businesses and the type and degree of risk.

Furthermore, based on the Japan Post Group Management Agreements, in addition to its own audit work, the Internal Audit Department of the holding company, Japan Post Holdings makes recommendations for improvement to the internal audit departments of Japan Post, Japan Post Bank, and Japan Post Insurance as necessary, and also conducts direct audits of those three companies.

Japan Post Group Basic Policy on Internal Auditing

Japan Post Group's Basic Policy on Internal Auditing is available for your viewing.

Internal audit activities that contribute to management

The Internal Audit Department of each Group company verifies the status of management activities and internal control systems in order to achieve the objectives stated in the basic policy. These results of this verification and the status of any subsequent improvements are compiled and reported to the Board of Directors, representative executive officers, Audit Committee, and Audit and

Supervisory Board, among others, to ensure that business improvements are made at each company.

In addition to individual verifications, we also work to conduct effective and convincing internal audits by attending various meetings, collecting internal management materials, and conducting interviews with individual departments to ascertain and deepen our understanding of individual operations and initiatives on a daily basis.

Furthermore, to ensure that the PDCA cycle for improving the quality of internal audits is functioning properly, the Audit Committee and Audit and Supervisory Board evaluate the development and operation of internal audit functions, and we work to make continuous improvements.